Gold has always been a paradoxical metal. It is both an anchor of stability and a barometer of uncertainty. And right now, the paradox is sharper than ever. In China, the world’s largest consumer of physical bullion, gold continues to trade at a discount to the London Bullion Market Association (LBMA) benchmark, closing last Friday nearly -0.9% below London prices. At the very same time, Shanghai vaults are reporting record-breaking inflows, with holdings now surpassing 66 tons (2.1 million ounces) — the highest level in history.

The combination is unusual, even contradictory: relentless inflows into vaults on one side, and persistent discounts on the other. The natural question is whether these dynamics foreshadow an inflection point in gold pricing — a structural tightening of supply, or merely a temporary dislocation between paper and physical markets.

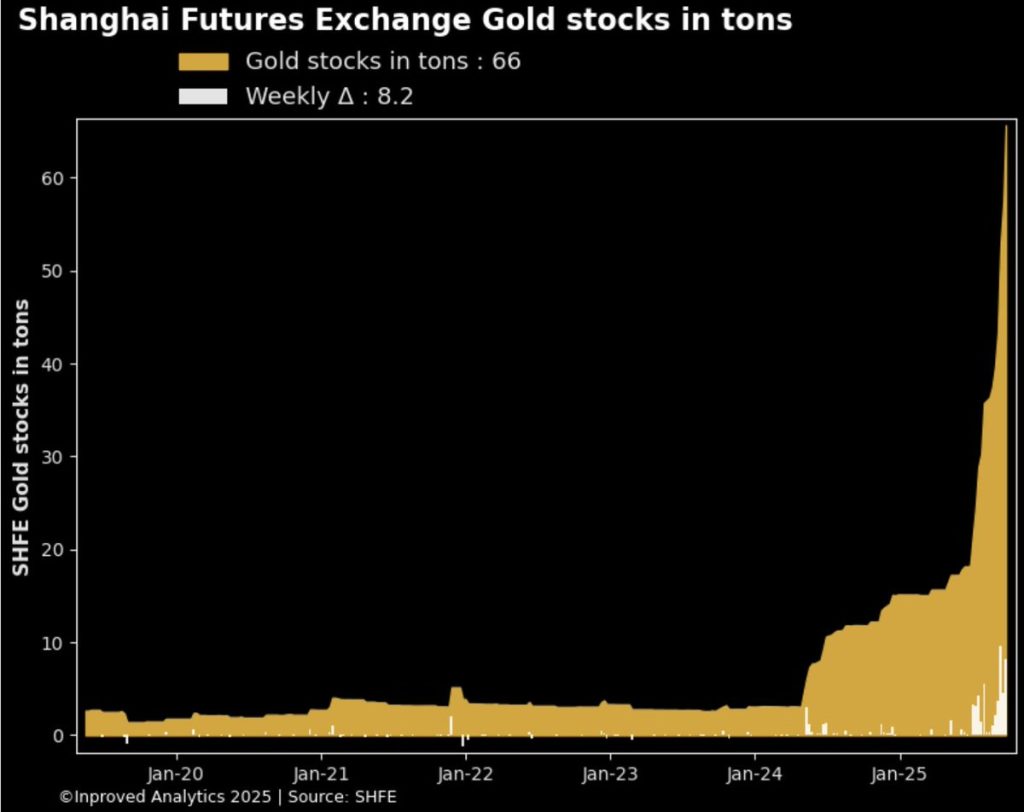

Shanghai: Discounts Amid Record Vault Inflows

The numbers out of China in late September are startling. The Shanghai Gold Exchange (SGE) and Shanghai Futures Exchange (SHFE) vaults absorbed 8.2 tons of gold in a single week, the second-largest weekly increase ever recorded. On Thursday alone, the inflow reached 5 tons, pushing total holdings to 66 tons, marking a staggering 260% year-to-date rise.

Yet despite these aggressive inflows, the local premium that usually signals strong demand flipped into discount. Gold in Shanghai has been trading between -0.7% and -0.9% below LBMA benchmarks, equivalent to a $25–35 per ounce discount.

This is not without precedent. During 2013, when China’s imports surged after prices collapsed, discounts persisted for months. More recently, in 2022, as capital controls tightened and yuan weakness weighed on investor sentiment, Shanghai premiums narrowed into discounts despite heavy vault buying.

Analysts point to two overlapping dynamics:

Policy and currency pressure – A weaker yuan and fragile domestic sentiment cap willingness to pay premiums.

Structural stocking – Steady inflows into SHFE vaults may be long-term stocking by state-linked entities rather than short-term jewelry demand.

In other words, the vault data suggests preparation for the long term, while the discount reflects hesitation in the present.

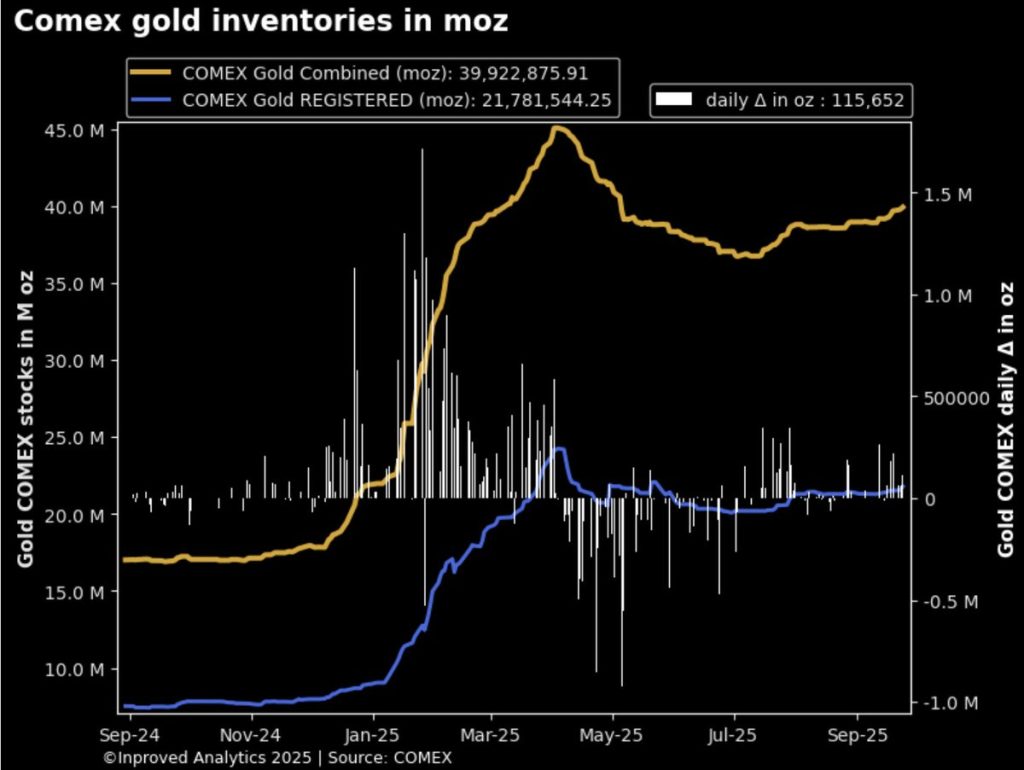

COMEX: New York Keeps Stacking

Across the Pacific, COMEX warehouses in New York are swelling again, with gold stocks climbing toward a five-month high of nearly 40 million ounces. Inflows of nearly 7 tons in a single week show that metal is steadily flowing into deliverable stockpiles, even as futures volumes remain heavy.

But here, too, the picture is more complex. Only a portion of those 40 million ounces sit in the registered category — deliverable metal for futures contracts. Eligible stocks, while physically present, may not be immediately available for delivery.

History has shown why this matters. In 2011, when gold surged to $1,920, COMEX appeared flush with inventory, but the registered portion had thinned dramatically. That mismatch amplified volatility once delivery demand surged. The same risk lurks today.

Lessons From Past Discount Cycles

2013: The Great Import Surge – Prices collapsed, imports soared, premiums vanished into discounts. It took months before premiums recovered.

2018–2019: Yuan Weakness – Discounts emerged during the trade war, flipping to premiums once the yuan stabilized.

2022: Lockdowns – Heavy vault inflows met weak retail appetite, keeping discounts alive until consumer sentiment turned.

In each case, vault inflows at discounts proved transitional. When macro or currency conditions stabilized, premiums came back — often heralding global rallies.

The Paradox of Premiums and Inflows

China is stacking gold at unprecedented levels, yet discounts persist. It’s as if two markets are coexisting: one in which long-term players hoard, another where short-term investors hesitate.

That tension cannot last forever. Either premiums will return as demand catches up, or inflows will slow. Historically, vault accumulation has been the truer signal.

Why It Matters Beyond China

Physical vs paper tension – Heavy vault inflows versus discounted prices sharpen the debate over whether “paper” markets suppress physical signals.

Policy signals – State-linked stocking aligns with the global trend of central banks diversifying into gold.

Catalyst potential – Discounts flipping into premiums have historically marked turning points for global gold rallies.

Guidance for Conservative Investors

For conservative investors — civil servants, matured PMETs, or those prioritizing steady wealth preservation — this environment is not a call to speculate but to act with discipline.

Discounts to LBMA are rare. In 2013, 2018, and 2022, investors who used these windows to gradually accumulate physical bullion preserved and later grew wealth. By contrast, those who waited for sentiment to improve often bought back in at higher premiums.

The “to-do list” today:

Treat discounts as opportunity — Current -0.7% to -0.9% discounts are effectively rare sale prices.

Accumulate gradually — Fixed monthly or quarterly allocations (5–10% of savings) mitigate timing risk.

Favor physical in Singapore — With zero capital gains tax, low acquisition premiums, and independence from capital controls, Singapore remains the region’s most efficient hub for conservative buyers, especially overseas Chinese and Indian investors.

Ignore futures noise — COMEX shorts and Shanghai discounts may spook traders, but they are cyclical. Physical allocation is the steady play.

As Hugo Pascal recently remarked, “Gold doesn’t care about today’s premium or discount. It cares about the direction of trust.” For conservative investors, that means measured accumulation while others hesitate.

Conclusion: The Calm Before the Premium

Gold at a discount in China while vaults overflow is not a contradiction — it’s a signal. History suggests such moments precede renewed premiums and higher global prices.

For long-term, conservative investors, this is the time to quietly keep stacking, using Singapore’s unique tax and vault advantages. When the discount finally flips, today’s buyers will already be positioned for the next leg higher.

Want to know more?

Talk to your consultants to pick their brains about Gold Prices.

Hugo Pascal’s observation about the AU9999 contract hitting a 10-week volume high underscores the increasing significance of physical gold trading on the Shanghai Gold Exchange. This trend not only highlights robust domestic demand in China but also reflects broader shifts in the global gold market toward physical-backed assets.